A Swiss spa buyer places a replenishment order for treatment oils, masks, and retail add-ons. The basket is healthy. The relationship is good. Then the practical question lands on your desk. Do you ask for prepayment, take a card, or let the client pay by invoice on terms?

For many Swiss B2B sellers, that choice isn't about checkout convenience. It's about how much trust you're willing to extend, how much admin your team can absorb, and whether your payment setup helps or hurts repeat ordering. In premium beauty, pharmacy, wellness, and clinic supply, invoice terms often sit right at the centre of the commercial relationship.

The businesses that handle pay by invoice well usually do two things. They treat it as a controlled credit process, not a casual payment option. And they adapt it to Swiss payment habits, digital invoicing standards, and buyer-side approval workflows instead of copying a generic e-commerce model.

Is Offering 'Pay by Invoice' Right for Your Business?

A common situation looks like this. A spa or pharmacy account orders regularly, prefers consolidated paperwork, and doesn't want staff using company cards for every replenishment. They want an invoice, a clear due date, and enough internal time to check goods against the order before paying.

That request is reasonable. In Swiss trade, invoice-based settlement remains embedded in how many businesses buy, approve, and pay. If you sell premium goods to professional customers, pay by invoice can improve account stickiness because it fits how buyers already operate.

But it only works when you know why you're offering it.

When it helps

Pay by invoice tends to work well when your buyers are repeat trade accounts with predictable order patterns and formal procurement habits. Pharmacies, clinics, spas, and established resellers often want documentation that can move cleanly through internal approval and bookkeeping.

It also suits purchases where the buyer expects to inspect the order, confirm quantities, and then release payment. That's very different from a one-off impulse purchase.

A good fit usually includes:

- Repeat ordering behaviour where the customer buys on a cadence you can monitor

- Professional buyers who need invoices for accounting, VAT handling, or internal sign-off

- Higher-value baskets where immediate card payment creates friction

- Operational discipline on your side, including credit rules, reminders, and escalation

When it hurts

Pay by invoice becomes expensive when it is offered too broadly. New accounts with no trading history, buyers who dispute line items frequently, and customers with weak internal purchasing discipline can turn one invoice into a chain of exceptions.

Practical rule: Offer invoice terms where they support a trading relationship. Don't use them as a default for every new account.

If you're reviewing your wider payment mix, it also helps to compare invoice terms with other top APMs for higher conversions. That kind of comparison forces a better question: which customers need trade credit, and which ones need a smoother way to pay?

Understanding B2B Invoice Payments and Terms

In B2B, pay by invoice is short-term trade credit. You ship goods or deliver services first, then give the buyer an agreed period to pay. That's not the same as consumer buy now, pay later. The logic is different, the risk is different, and the admin burden is yours unless you outsource it.

For trade accounts, invoice terms are part of the commercial deal. They affect purchasing power, stock planning, and supplier loyalty. For the seller, they affect cash timing and exposure.

What payment terms actually mean

When businesses use terms such as Net 30 or Net 60, they're agreeing on a payment window counted from the invoice date or another defined trigger in the contract. The exact number of days you offer should reflect your margins, order frequency, and customer reliability.

The mistake many suppliers make is treating terms as a sales concession only. They're not. Terms are a credit decision.

Think of invoice terms as a narrow, revocable credit line tied to trading behaviour. The line exists because the customer orders consistently, pays consistently, and sends clean purchase instructions. When one of those conditions fails, the line should change.

Why invoice quality matters as much as payment terms

In Swiss commercial practice, invoice-based terms like net payment windows are common. Enterprise procurement guides also make one point very clear. Correct invoice fields are what trigger approval. If the invoice includes the PO number and itemised goods, the buyer can auto-match it and release payment on schedule. If not, it can stall in validation and extend days-sales-outstanding, as noted in HighRadius on invoice payment workflows.

That means your commercial terms and your invoice structure can't be separated.

A workable B2B invoice usually needs:

- Clear supplier identity so AP can recognise the vendor without guesswork

- Invoice number and date that match the buyer's recordkeeping rules

- Due date and payment terms stated plainly, not buried in fine print

- PO reference where applicable because many buyers won't approve without it

- Itemised lines showing what was supplied, in what quantity, and at what price

- Tax-relevant detail so the buyer's finance team can post it correctly

If a customer says they “pay by invoice”, what they often mean is “our accounts payable team will pay a correctly documented invoice after verification”.

A practical term-setting approach

Don't give every account the same terms. Segment them.

| Customer type | Better starting position | Why |

|---|---|---|

| New trade account | Prepayment or very tight invoice terms | No payment history yet |

| Established repeat buyer | Standard invoice terms | Relationship and ordering pattern support it |

| Account with disputes or late approvals | Shorter terms or order hold | Exceptions create hidden credit cost |

| Large strategic account | Terms linked to PO discipline and order process | Volume can justify credit if process is controlled |

That approach keeps invoice terms commercial rather than sentimental.

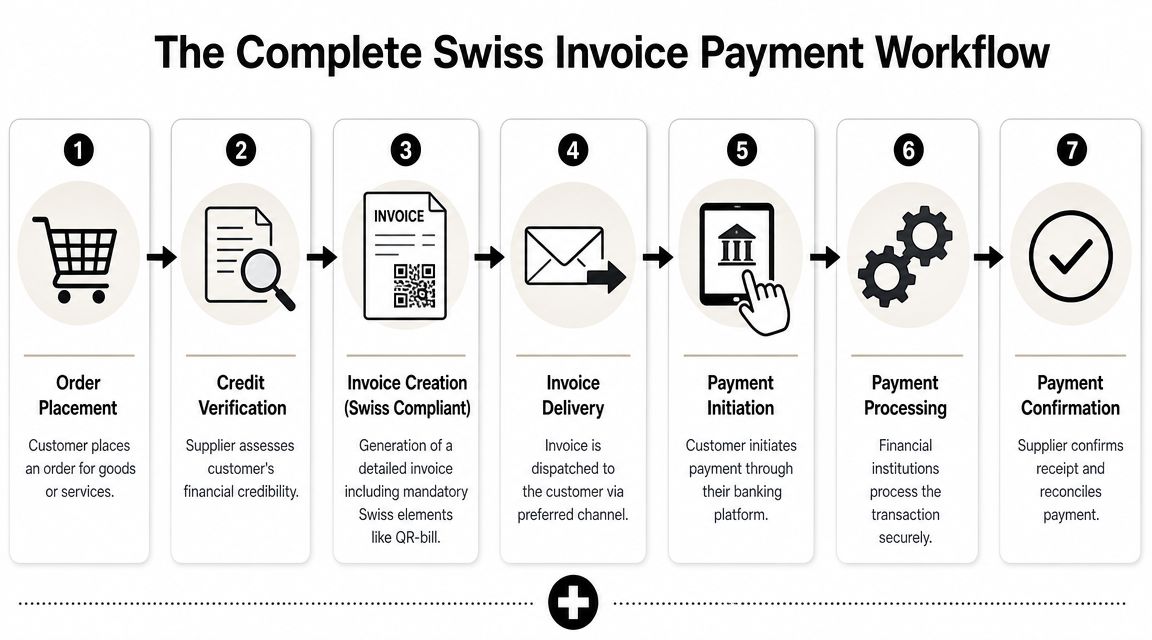

The Complete Invoice Payment Workflow in Switzerland

The Swiss invoice cycle is manageable when every handoff is deliberate. Problems usually start when sellers think the job ends at “send invoice”. It doesn't. The job ends when cash is matched, posted, and cleared with no loose ends.

This workflow visual sums up the process most Swiss B2B sellers need to control.

The seven stages that matter

Order placement

The buyer sends an order, often with a PO, named products, quantities, branch delivery details, and agreed pricing. If the PO is incomplete at this point, the payment problem has often already started.Credit verification

Before you confirm invoice terms, check whether this buyer should receive them. Existing account history matters more than optimism. For new customers, basic verification of business identity, billing contact, and order plausibility goes a long way.Invoice creation

Swiss specificity plays a significant role. The Swiss Interbank Clearing system and the shift to QR-bill standards were designed to standardise invoice payments, and the QR-bill became the mandatory invoice and payment slip format in Switzerland on 30 June 2020, replacing the old orange and red slips, as described in the Swiss QR-bill transition note. That change matters because it reduces manual reference errors and makes reconciliation easier.Invoice delivery

Send the invoice through the channel the buyer uses. Email may be acceptable for some accounts. Others need invoices routed into a portal, AP inbox, or banking-linked workflow.Payment initiation

The buyer's finance team or authorised staff member initiates payment. In Switzerland, that often means bank-led execution rather than card settlement.Payment processing

Once the payment is launched, the banking rails do the transfer. At this stage, reference quality matters. If payment data doesn't map back cleanly to the original invoice, your finance team loses time chasing avoidable mismatches.Payment confirmation and reconciliation

Funds arrive. Then your team confirms settlement against the right invoice and closes the loop in the accounting system.

What works in practice

The strongest Swiss setups are not the flashiest. They're the ones with predictable data and disciplined routing.

Good practice usually includes:

- One source of truth for customer terms so sales and finance aren't promising different things

- Consistent QR-bill formatting on every eligible invoice

- Named AP contacts at the customer's side for invoice delivery and disputes

- Fast exception handling for quantity differences, damaged goods, or missing PO references

A lot of firms also borrow ideas from invoice automation projects outside Switzerland. Even when the market context differs, the workflow thinking is useful. A practical example is this overview of UK business invoice automation, which is worth reading for process design, approval routing, and exception handling ideas.

Where the workflow usually breaks

Late payment often starts much earlier than the due date. It starts when the invoice can't move cleanly through the buyer's approval path.

The usual failure points are simple:

- The wrong billing entity appears on the invoice

- The PO number is missing

- Delivery and invoice details don't match

- Someone sends a PDF to a sales contact instead of AP

- A dispute sits in email with no owner

If you tighten those points, pay by invoice becomes much more predictable.

Managing Financial Risk and Preventing Fraud

The hard question with pay by invoice isn't whether customers like it. They usually do. The hard question is who carries the risk once the goods have left your warehouse.

In Switzerland, that's the under-discussed part. The biggest unanswered question around pay by invoice is who absorbs the invoice risk and admin burden after the sale. For beauty distributors and similar wholesale suppliers, a key concern is whether invoicing can be offered without increasing working-capital strain, especially when invoice exceptions create delays and AP disputes. That framing is captured well in this discussion of invoice exceptions and admin burden.

Risk control is not optional

Many suppliers treat risk management as something they'll formalise later, once invoice volume grows. That's backwards. If you don't define credit rules at the beginning, your team ends up improvising with each overdue account.

A workable control framework has four parts.

Customer onboarding

Before you approve invoice terms, confirm who you're dealing with. Make sure the business entity, billing address, delivery site, and purchasing contact all line up. If the order is unusually urgent, unusually large for a first transaction, or oddly inconsistent with the buyer's normal profile, pause it.

Credit boundaries

Set a clear maximum exposure for each account. That limit should include open invoices, not just the current order. If an account repeatedly runs close to the ceiling, that's a signal to review terms rather than keep extending trust by habit.

Reminder discipline

Dunning should be structured, polite, and consistent. Don't leave reminders to whichever team member happens to notice a late invoice.

A sensible rhythm often includes:

- Pre-due reminder for active accounts that appreciate advance notice

- Due-date follow-up confirming the invoice is scheduled

- Overdue reminder that names the invoice, amount due, and expected payment action

- Escalation path if the delay is caused by dispute, missing documentation, or silence

If you need a practical framework for escalation steps and communication tone, GenerateSEPA's debt collection guide is a useful operational reference.

Fraud and abuse signals to watch

Not every bad invoice outcome is fraud. Some are just poor procurement habits. Still, a few signs deserve attention:

Mismatch between business identity and delivery request

For example, the billing entity looks established, but the delivery instruction changes repeatedly or points to an unrelated contact.Pressure for urgent release of goods before account checks are finished

Real buyers can be urgent. Fraudsters often weaponise urgency.Resistance to standard documentation

A legitimate B2B buyer rarely objects to supplying routine business details.Repeated disputes on basic facts

If a customer regularly contests obvious line items or agreed charges, the issue may be process weakness, not misunderstanding.

Decision rule: When exceptions become a pattern, don't just chase payment. Reassess whether the account should stay on invoice terms at all.

When to switch to prepayment

Many suppliers hesitate for too long. If one invoice goes late because AP was slow, that's manageable. If an account repeatedly causes disputes, misses agreed steps, or leaves reminders unanswered, you should consider moving them to prepayment or a more controlled payment rail.

That is not punitive. It is portfolio management.

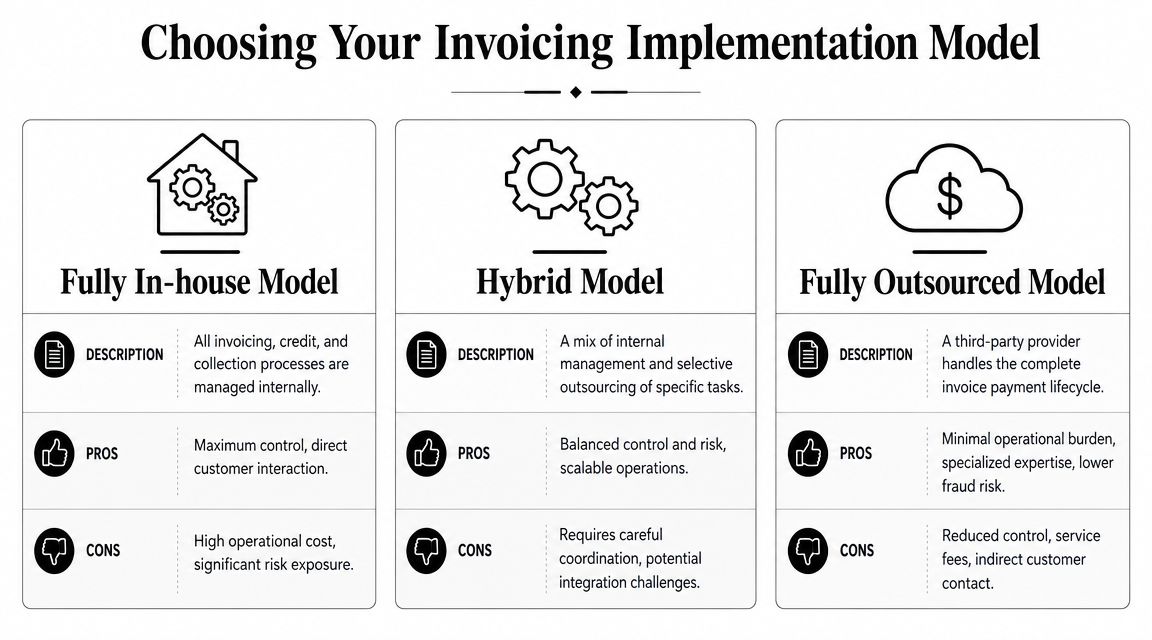

Choosing Your Invoicing Implementation Model

There isn't one correct way to offer pay by invoice. The right model depends on how much control you want, how much operational burden your team can carry, and how much risk you're prepared to keep on your own balance sheet.

This comparison is the most useful place to start.

For Swiss merchants, the practical decision is broader than “should we offer invoices”. The more strategic question is which payment rails are fastest and cheapest, especially as expectations for digital and instant-style payments rise. That shift is why many firms now compare classic invoice terms with pay-by-bank and direct-debit options for higher-value B2B accounts, as discussed in this analysis of faster invoice payment strategies.

Model one: fully in-house

In this setup, your business manages everything. Credit checks, invoice issuance, reminders, disputes, and collection all stay internal. You might use accounting software, ERP workflows, and your own finance team, but the responsibility is still yours.

This model suits businesses that want tight customer control and already have strong finance operations.

Best when:

- You know your customer base well

- Your order volume is manageable

- Your team can enforce credit policy consistently

Main upside: You own the customer relationship end to end.

Main downside: You also own every late payment, exception, and admin task.

Model two: hybrid

A hybrid setup keeps key decisions in-house but outsources selected tasks. For example, you may approve which accounts get invoice terms, while a software platform handles invoice delivery, reminders, payment links, or bank-based collection options.

For many SMEs, this is the most practical middle ground. It reduces repetitive admin without handing away the full customer experience.

Examples of a hybrid approach include:

- Using accounting software to generate invoices while automating reminders

- Keeping credit approval internal but using a provider for digital presentment

- Moving certain high-risk accounts to direct debit while leaving trusted accounts on traditional invoice terms

Model three: fully outsourced

In a fully outsourced model, a third party manages most or all of the invoice payment lifecycle. Depending on the provider, that can include credit decisioning, payment collection, reminder flows, and sometimes risk absorption.

This route is attractive when your sales team wants to offer invoice terms broadly but your finance team doesn't want the operational load.

The trade-off is obvious. You gain speed and lower internal burden, but you lose some control over customer communication, acceptance criteria, and commercial flexibility.

Side-by-side comparison

| Model | Control | Admin effort | Risk exposure | Customer experience |

|---|---|---|---|---|

| Fully in-house | High | High | High | Very flexible if your team is organised |

| Hybrid | Medium to high | Medium | Medium | Usually the best balance for growing B2B sellers |

| Fully outsourced | Lower | Lower | Lower, depending on provider terms | Smooth if provider fits your customers' buying habits |

How to choose without overcomplicating it

Ask four direct questions.

Who knows the customer best

If your sales and finance teams have long-standing account knowledge, keeping credit decisions in-house often makes sense. If your customer base is broader and less predictable, external support may be safer.

Where does your team already struggle

If invoices go out on time but reminders don't, a hybrid model may solve the bottleneck. If credit review is weak from the start, no amount of reminder automation will fix that.

Which accounts deserve classic invoice terms

Not every buyer needs the same rail. Strategic repeat accounts may justify invoice terms. Other customers may be better served with direct debit, pay-by-bank, or prepayment.

What experience do buyers expect

Professional Swiss buyers increasingly expect digital efficiency, but they still care about familiar account-based settlement. The implementation model should preserve both.

A good invoicing model doesn't just collect money. It tells you which customers deserve more trust, which ones need tighter controls, and which ones should move to a different payment method.

Sample Policies and Wording for Your Website

Most payment problems begin long before the due date. They begin when your website, account application, and invoice emails leave too much unsaid. Good policy wording won't eliminate disputes, but it will reduce ambiguity and give your finance team something solid to point back to.

This checklist is a useful way to think about the minimum policy layer around pay by invoice.

Sample payment method wording

Use plain language. A professional buyer shouldn't have to decode your terms.

Payment by invoice is available to approved business customers only. Invoice eligibility is subject to account review and may vary by order history, order value, and account status. Unless otherwise agreed in writing, payment is due within the period stated on the invoice. We reserve the right to require prepayment or an alternative payment method for new accounts, overdue accounts, or orders that fall outside an approved credit profile.

That wording does three useful things. It limits invoice access to approved B2B accounts, ties eligibility to account status, and preserves your right to change the method later.

Sample credit eligibility policy

This belongs on an application form, trade account page, or terms document.

Business status required

Invoice terms are offered to registered business customers purchasing for commercial use.Account review applies

New customers may be asked to provide billing details, delivery details, and a named finance or purchasing contact.Approval is conditional

Invoice terms can be changed, suspended, or withdrawn if payment delays, repeated disputes, or documentation issues occur.Order release remains discretionary

Orders may be held pending payment confirmation where account activity falls outside agreed terms.

Reminder email templates

Short beats dramatic. Use specific invoice references and a clear next step.

Due soon

Subject: Upcoming invoice due date

Dear [Customer Name],

A quick reminder that invoice [Invoice Number] is due on [Due Date]. If payment is already scheduled, no action is needed. If you need a copy invoice or have a query on the order, please reply to this email.

Kind regards,

[Company Name]

Just overdue

Subject: Invoice [Invoice Number] is now overdue

Dear [Customer Name],

Our records show that invoice [Invoice Number], dated [Invoice Date], remains unpaid. Please confirm the payment date or let us know today if there is any issue with the invoice details, delivery, or approval process.

Kind regards,

[Company Name]

Escalation stage

Subject: Action required on overdue invoice [Invoice Number]

Dear [Customer Name],

We have not yet received payment or an agreed payment date for invoice [Invoice Number]. Please send confirmation of payment status today. If there is an approval issue or dispute, please identify the point requiring review so we can address it promptly. Continued delay may affect future orders being released on invoice terms.

Kind regards,

[Company Name]

Return and dispute wording

Return and dispute handling should connect tightly to invoicing.

A practical website line is:

Any discrepancy in delivered goods, pricing, or invoice details should be reported promptly to your account contact or our finance team, with the relevant invoice number and product details. Undisputed amounts remain payable in line with agreed terms.

That final sentence matters. It stops a small issue from freezing an entire balance.

Swiss VAT and Accounting Best Practices

Pay by invoice only stays efficient when the invoice is complete enough to move cleanly through bookkeeping, VAT handling, and buyer approval. In Switzerland, invoice completeness is not an administrative nicety. It is a processing requirement.

The Swiss eBill model points in the right direction here. It is designed to deliver invoices digitally into the recipient's finance workflow, and structured invoice data for supplier identity, invoice number, due date, and VAT-relevant amounts reduces manual keying, shortens dispute cycles, and avoids payment delays, as outlined in the electronic invoice standards reference.

What your invoice should support

Your invoice has to do more than request payment. It should support four parallel needs:

- Buyer approval so AP can validate it without chasing clarifications

- VAT handling so tax-relevant fields are visible and consistent

- Ledger posting so your own accounting team can record it correctly

- Audit readiness so the documentation trail holds up later

If you use systems such as Bexio, Abacus, or another accounting platform, the principle is the same. The cleaner your source data, the less manual repair work your team will do later.

Practical bookkeeping habits

Keep the process disciplined.

Match invoice issue dates and supporting records

The invoice date, delivery record, and order record should tell the same commercial story. If your warehouse record says one thing and your invoice says another, reconciliation turns into detective work.

Keep VAT-relevant detail structured

Don't bury tax-relevant values in free-text notes. Put them in fields your system and the buyer's system can read and post correctly.

Separate disputes from settled facts

If part of an order is in dispute, document the reason clearly. Don't leave the whole transaction vague in your ledger.

Clean accounting starts with clean commercial documents. Finance teams can't automate around messy source data forever.

What usually causes avoidable accounting friction

| Problem | Likely result |

|---|---|

| Missing invoice number or inconsistent numbering | Posting confusion and delayed matching |

| Weak product line detail | Buyer disputes and difficult VAT review |

| Missing due date or unclear terms | Delayed scheduling and reminder confusion |

| Unstructured data in PDF-only workflows | More manual keying and avoidable errors |

If you want smoother VAT handling, cleaner month-end close, and fewer payment delays, start with invoice design rather than chasing issues after posting.

Frequently Asked Questions for Merchants

What should I do if a B2B customer disputes an invoice?

Separate the disputed point from the undisputed balance straight away. Confirm whether the issue is pricing, quantity, delivery condition, missing PO reference, or billing entity mismatch. Assign one owner internally and one contact at the customer side. If the customer accepts most of the invoice, don't let the whole balance drift into limbo.

Should my return policy differ for pay by invoice orders?

Yes, at least operationally. Your return and dispute rules should be clearer, because the payment is still outstanding while the issue is being reviewed. State how customers should report discrepancies, which references they must include, and whether undisputed amounts remain payable during the review.

Can I charge late fees or default charges?

You should take local legal and contractual advice before applying charges. In practice, the safer business habit is to define payment terms, reminder timing, and escalation rights clearly in your account terms before an overdue event happens. Ambiguity causes more friction than firmness.

How do I handle partial payments?

Post them against the exact invoice and contact the customer immediately to confirm whether the shortfall is deliberate or accidental. Partial payments often reveal a dispute that no one formally raised. If your team ignores that signal, the remaining balance becomes harder to recover.

When should I stop offering invoice terms to a customer?

Look for patterns, not isolated incidents. A single delay may reflect an AP bottleneck. Repeated late approvals, recurring disputes, missing remittance information, or silence after reminders usually mean the account needs tighter terms, prepayment, or a different payment method.

Is pay by invoice still worth offering if digital payment options are improving?

Often yes, but not for every account. For many Swiss B2B buyers, invoice terms still fit internal purchasing and approval habits. The smarter move is not choosing one method for everyone. It's segmenting customers so trusted accounts stay on invoice terms while other accounts move to lower-friction, lower-risk digital rails.

What's the simplest way to improve pay by invoice performance without changing provider?

Tighten the basics first:

- Use consistent invoice fields so buyers can process the document quickly

- Require PO references where relevant before the invoice is issued

- Name a finance contact for disputes and remittance questions

- Automate reminders so no invoice depends on memory

- Review exceptions monthly to identify which customers are consuming the most admin

That short list fixes more than most software changes.

If you're a Swiss pharmacy, spa, retailer, or wellness business looking to strengthen your premium assortment while working with a distributor that understands compliance, structured trade relationships, and the realities of Swiss B2B commerce, explore beautysecrets.agency. Their portfolio and market focus are built for professional partners who need more than attractive products. They need reliable supply, credible brand positioning, and a trade setup that works in practice.